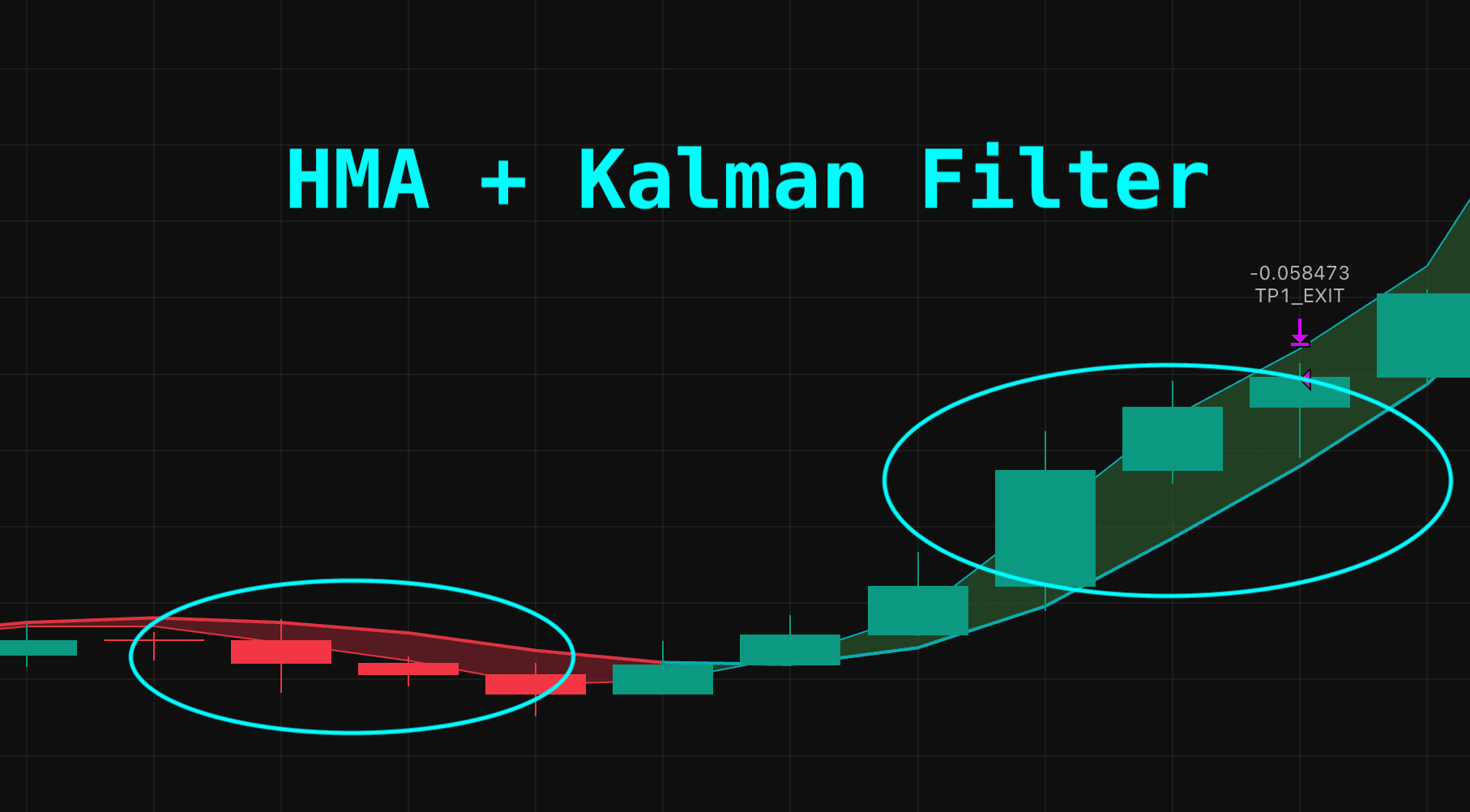

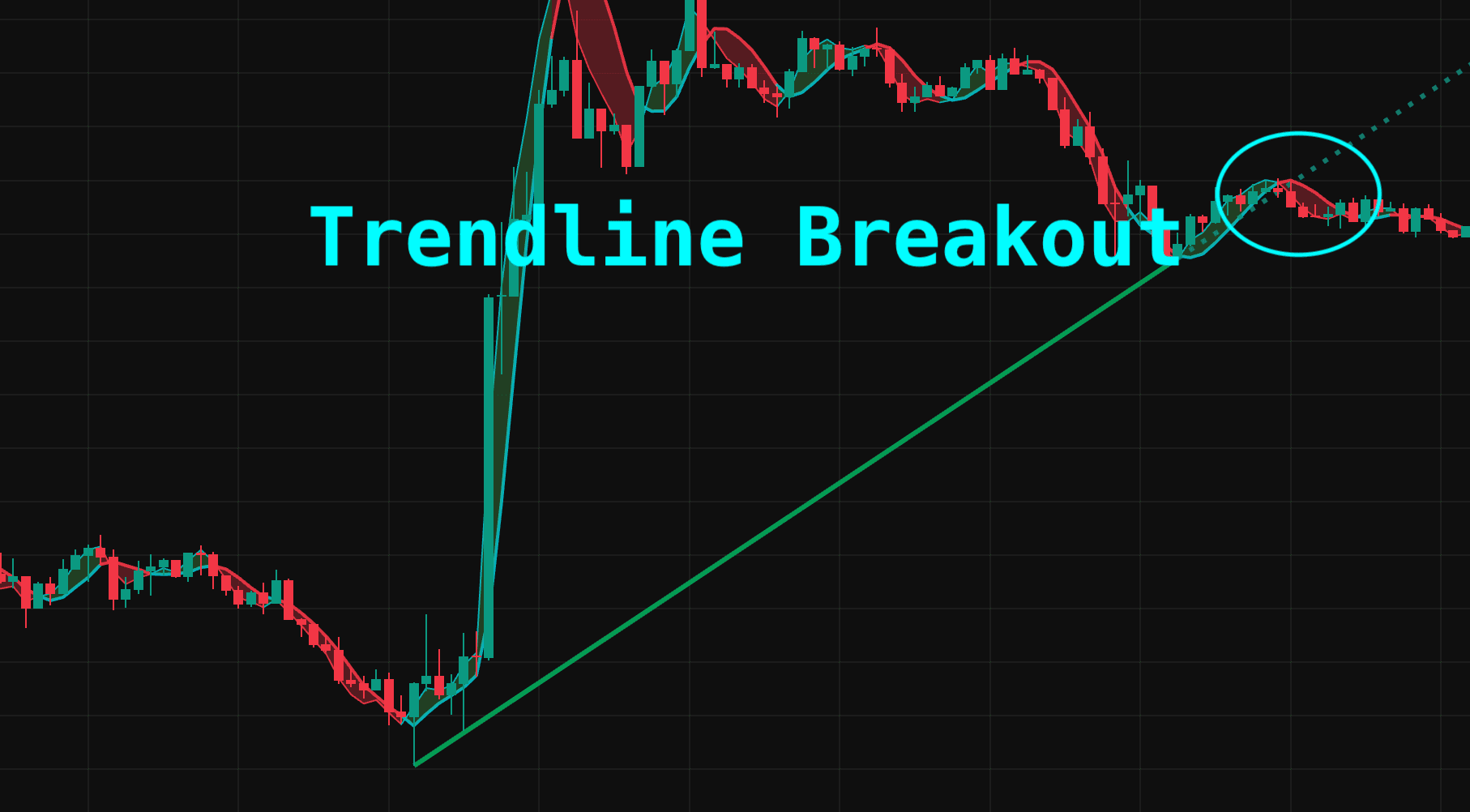

Trend Break Sync Strategy is a trend-following strategy inspired by Kalman Filter–based data filtering concepts used in aerospace and engineering fields. By synchronizing the cross of two smoothed lines (Line A & B) created from HMA (Hull Moving Average) combined with a Kalman filter with Trendline Breakouts, the strategy aims to capture high-probability entry points.

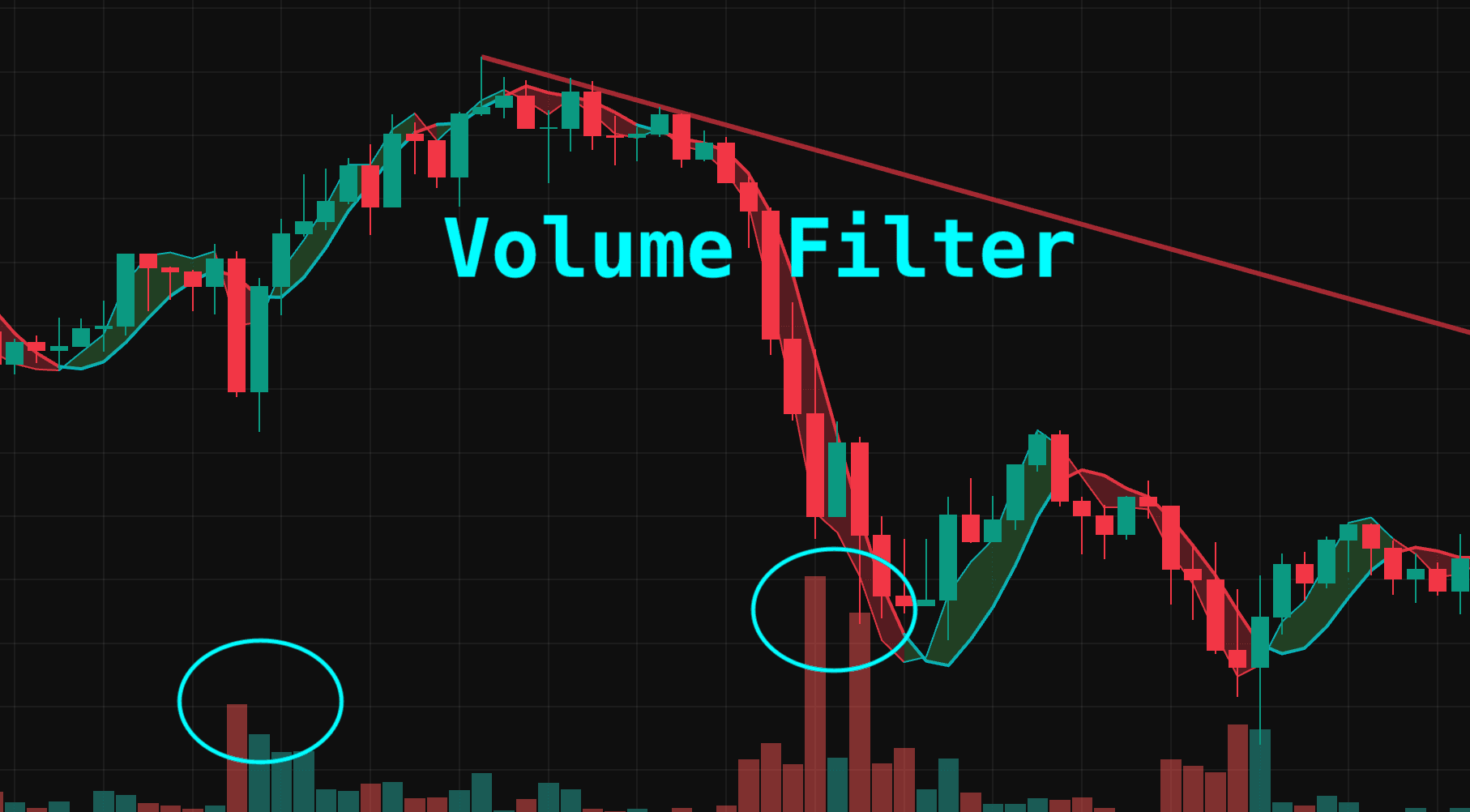

Rather than relying on a simple moving average crossover, this strategy integrates trend reversal signals, trendline breakouts, volume confirmation, and breakout strength scoring to reduce noise signals and enter only when a meaningful structural shift in the market is likely occurring.

The Kalman Filter is originally an algorithm used in aerospace and engineering to estimate real movement from noisy sensor data. By applying this concept to market data, the strategy filters out price noise and captures actual trend changes more reliably.

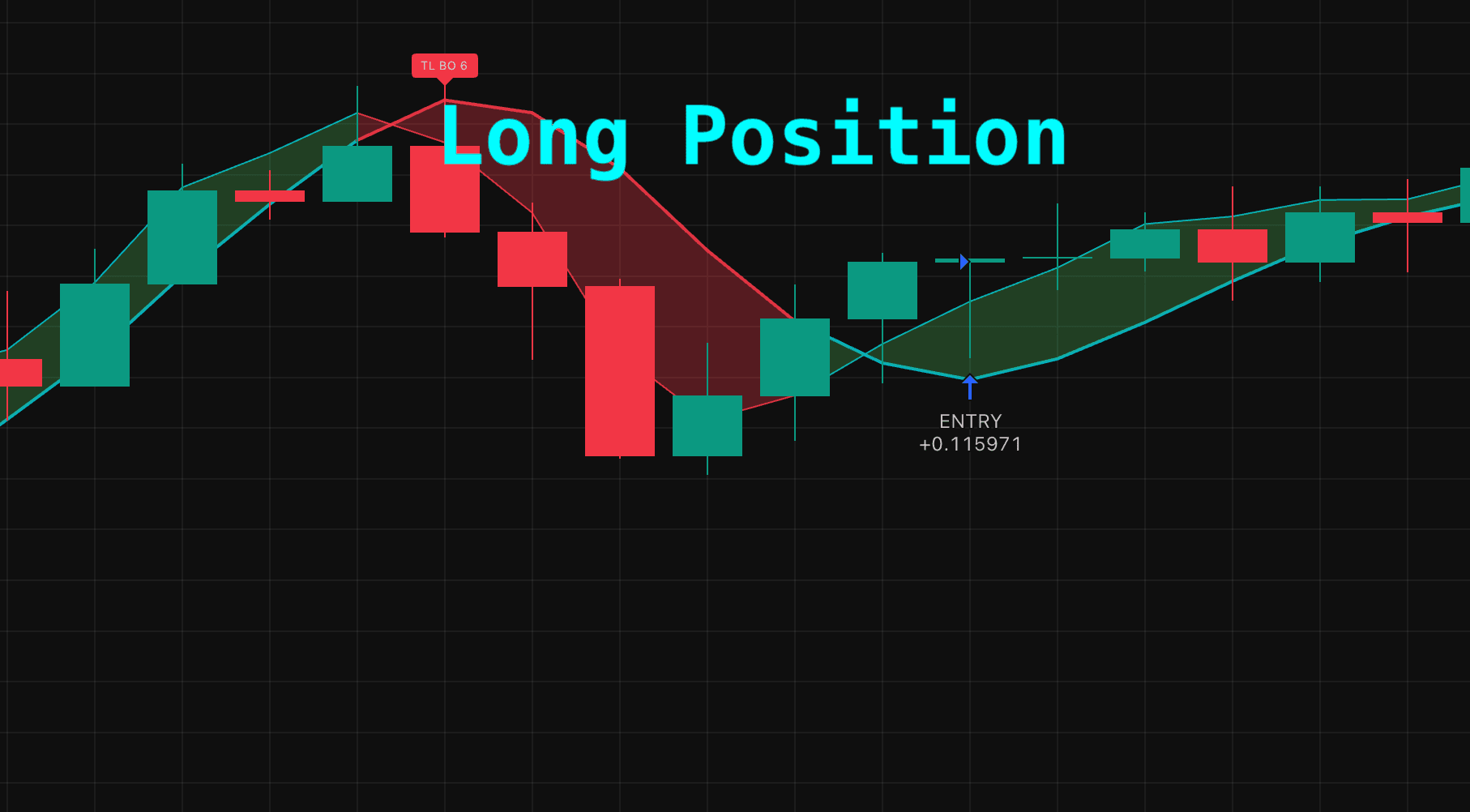

Backtest results show:

- Average win rate: 55–60%

- Average return per trade: around 20%

This demonstrates that the strategy performs efficiently by focusing entries on areas where trend reversals and structural breakouts occur simultaneously.